Global AI investment hit $211B in 2025, surging 85%. See who's leading, where capital flows, and what's next for the AI funding boom.

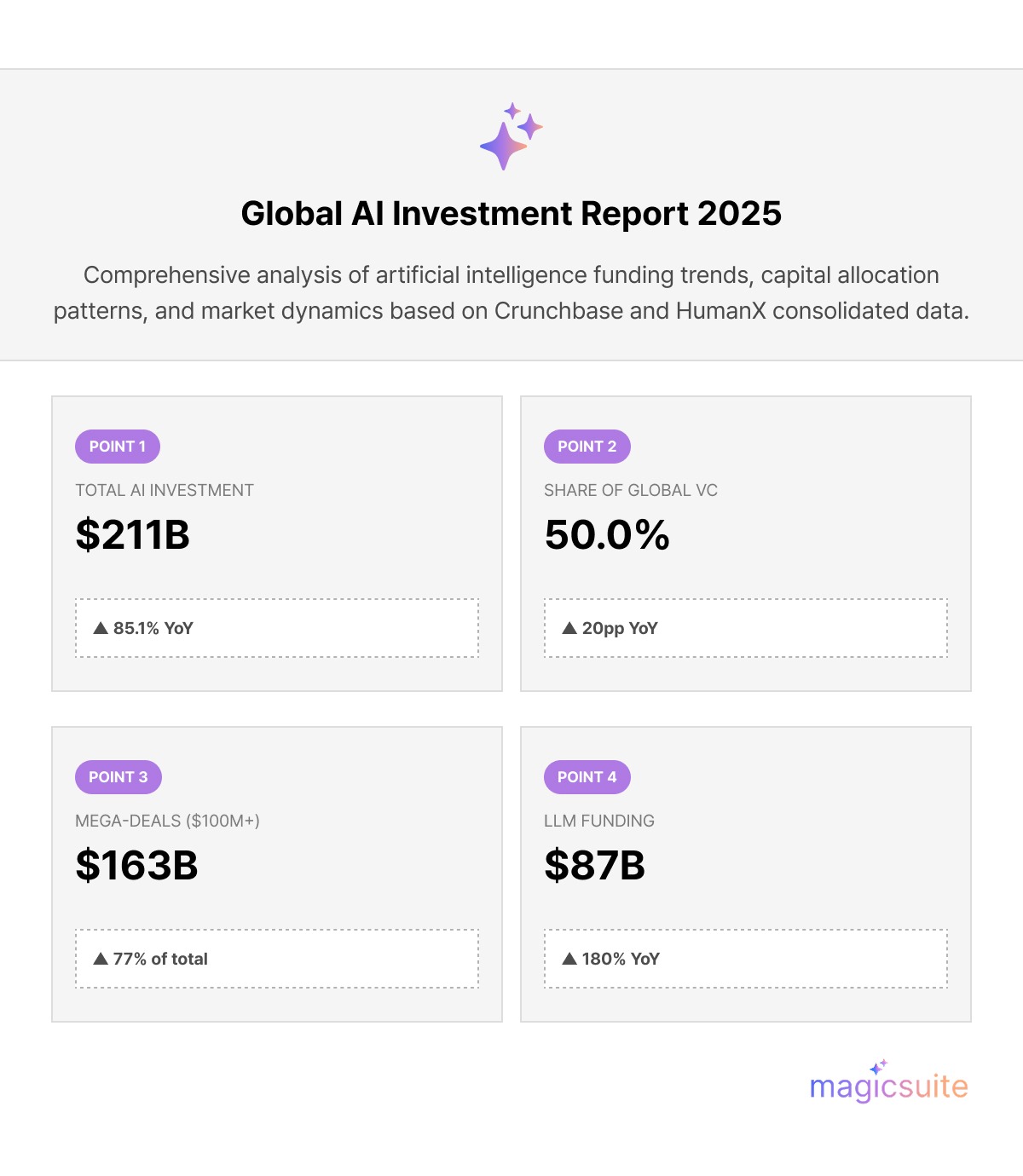

The global race for artificial intelligence supremacy reached a historic fever pitch in 2025. According to the 2025 AI Funding Report, jointly released by data analysis firm Crunchbase and global AI conference operator HumanX on January 31, 2026, AI-related companies worldwide attracted a staggering $211 billion in funding last year.

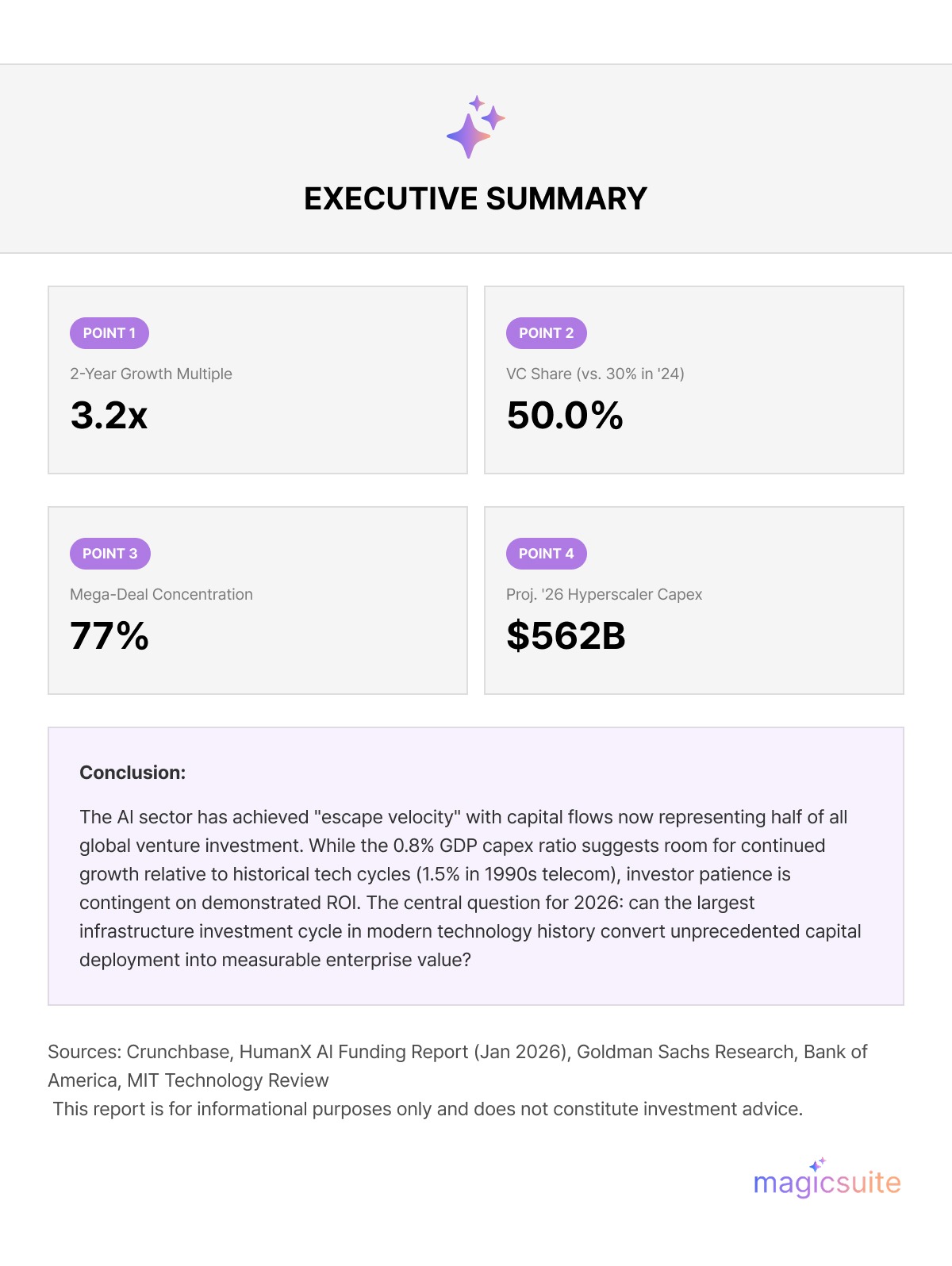

This massive capital influx represents an 85% surge from the $114 billion raised in 2024 and a nearly threefold increase from the $65 billion recorded in 2023. By nearly doubling its previous annual record, the AI sector has reached what analysts describe as "escape velocity," now accounting for 50% of all global venture capital investment.

The headline figure of $211 billion marks a decisive shift in the financial landscape. To put this in perspective, AI investment has more than tripled in size in just two years. "Last year, AI actually became the standard for startup investment," the report states. Investors are no longer treating AI as a "sub-sector" but as the foundational layer for all new enterprise technology.

This explosion in funding is driven by the realization that AI is not a fleeting trend but a core utility. In 2025, approximately half of global venture capital flowed into AI companies. This "black hole" effect has left other sectors—such as traditional SaaS, fintech, and consumer apps—scrambling for the remaining 50% of the VC pool.

The most significant trend of 2025 was the intensifying concentration of capital. We are seeing a market in which a small elite group of companies monopolizes most of the funding.

In 2025, 77% of all AI funding—totaling $163 billion—went to companies raising rounds of $100 million or more. This is a sharp increase from 67% in 2024. Investors are no longer casting a wide net; they are placing massive, high-conviction bets on "proven" winners.

Companies developing Large Language Models (LLMs) accounted for 40% of the total ($87 billion), a 180% year-over-year increase. Two industry leaders alone—OpenAI and Anthropic—secured $58.5 billion combined.

Crunchbase CEO Jagger McConnell noted, "Investors are selectively betting on companies that have proven their actual performance. They are no longer throwing money at anything simply labeled 'AI'." This discipline marks the transition from "AI hype" to "AI execution."

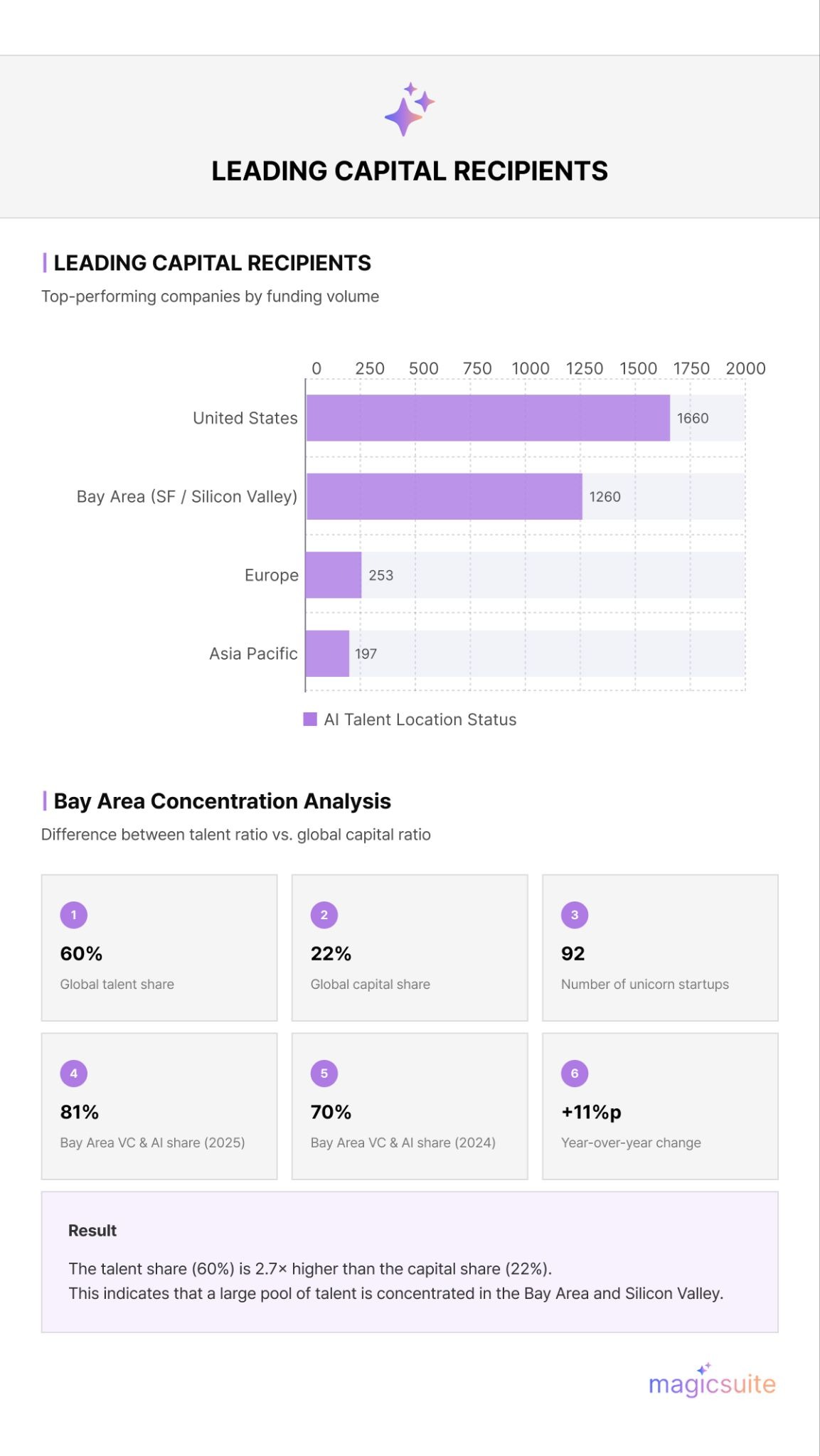

Geographically, the "push phenomenon" has reached its peak in the San Francisco Bay Area. The Bay Area, encompassing San Francisco and Silicon Valley, emerged as the undisputed "global control center" for the AI revolution. Last year, the region attracted $126 billion, representing 60% of all global AI investment. Remarkably, AI now accounts for 81% of all startup investment in the Bay Area, a jump from 70% in 2024.

However, while the Bay Area accounted for 60% of the money, it accounted for only 22% of global deals. This confirms that while innovation is occurring everywhere, capital is being hoarded by a small group of elite Silicon Valley firms. In fact, 92 companies in the Bay Area raised rounds of $100 million or more in 2025 alone. On a broader scale, the United States remains the primary engine of AI growth. U.S.-based companies received $166 billion, or 79% of the global total. While Europe and Asia saw growth in their respective AI sectors, the sheer scale of American capital remains unmatched.

The AI boom is no longer restricted to the laboratory or the chat window. It is driving a massive industrial expansion across the "picks and shovels" of the digital age. The remaining 59% of investment (roughly $124 billion) was distributed across:

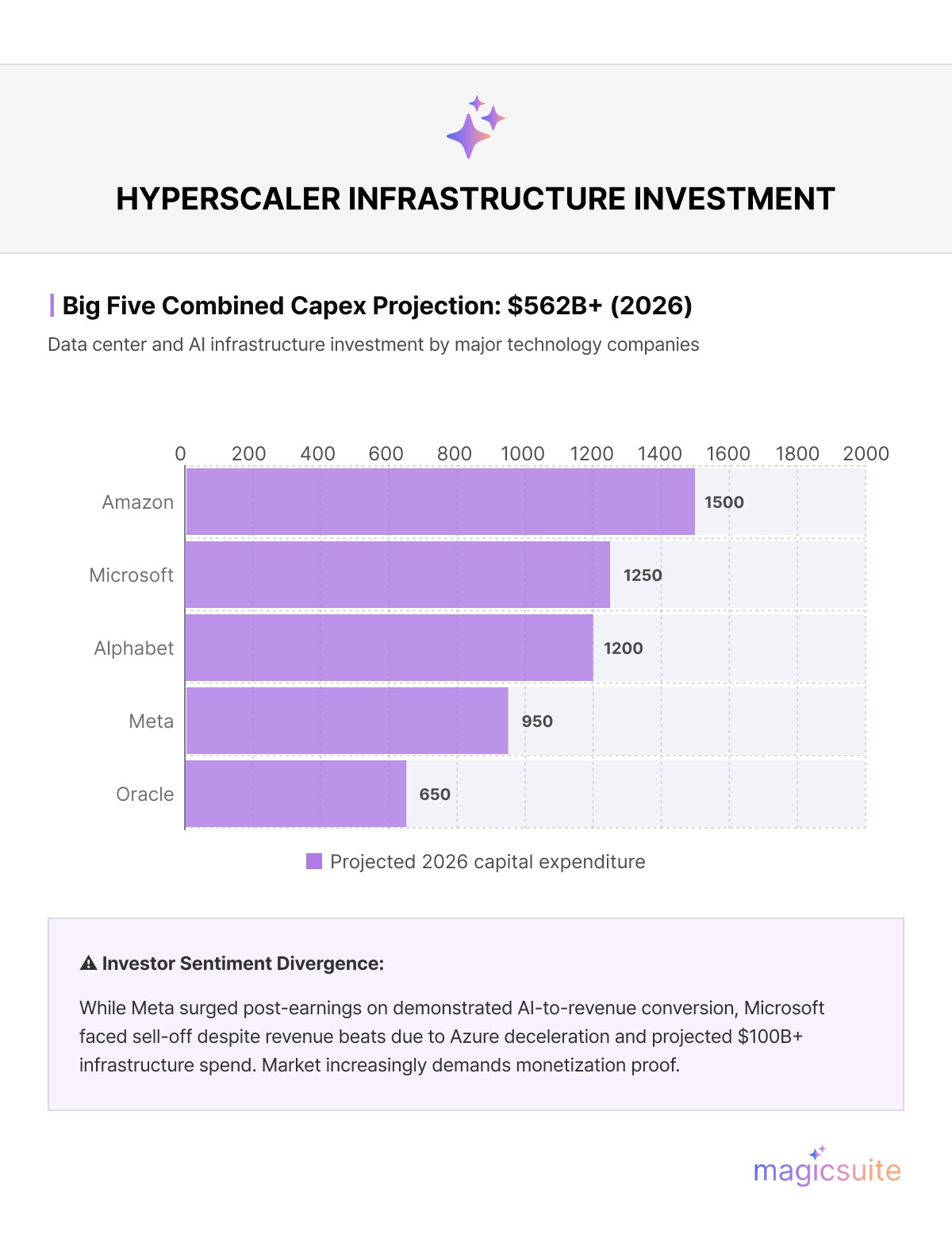

The world’s largest tech companies, the "hyperscalers," are pouring unprecedented sums into AI infrastructure. Wall Street analysts project that capital expenditures (capex) from the Big Five—Amazon, Microsoft, Alphabet, Meta, and Oracle—will exceed $562 billion in 2026.

Bank of America has described the current environment as a "supercycle similar to the boom of the 1990s," as companies race to build data centers that will house the intelligence of the future.

Despite the record-breaking figures, 2025 ended with questions about sustainability. Wall Street analysts project that Big Tech infrastructure spending (capex) will top $500 billion in 2026, yet investor patience is wearing thin for companies that cannot show immediate returns.

While Meta saw its stock surge after proving that AI improved its advertising engine, Microsoft faced a sharp sell-off despite beating revenue estimates. Investors were spooked by Azure’s slowing growth and the company's forecast to spend over $100 billion this year on infrastructure.

"We're firmly in an era where the monetization of AI capex has to be realized for the valuations of tech stocks to be justified," said Josh Chastant, portfolio manager at GuideStone Funds.

Adding to the caution, an MIT study found that 95% of generative AI pilot programs fail to achieve business value, and only 5% of enterprises report a significant impact on earnings.

Goldman Sachs notes that AI capex currently represents about 0.8% of U.S. GDP, still well below the 1.5% level seen during the late 1990s telecom boom. This suggests there may still be room for growth, provided companies can bridge the gap between "impressive demos" and "enterprise value." The HumanX report remains bullish for the near term, forecasting that 2026 will be a year of exits.

As we move into 2026, the "AI Revolution" is no longer just a technological story—it is a financial one. The world has placed a $211 billion bet on a smarter future. Now, it is time for the winners to pay out. The central question for the coming year is whether the largest capital-spending cycle in modern tech history can produce measurable returns before the market loses patience. For now, the "global control center" in Silicon Valley remains the heart of a $211 billion gamble on the future of intelligence.

Is this a bubble or a foundational shift? Goldman Sachs notes that AI capex currently represents about 0.8% of U.S. GDP, still well below the 1.5% level seen during the late 1990s telecom boom. This suggests there may still be room for growth, provided companies can bridge the gap between "impressive demos" and "enterprise value." As we move into 2026, the "AI Revolution" is no longer just a technological story—it is a financial one. The world has placed a $211 billion bet on a smarter future. Now, it is time for the winners to pay out.

Hanna is an industry trend analyst dedicated to tracking the latest advancements and shifts in the market. With a strong background in research and forecasting, she identifies key patterns and emerging opportunities that drive business growth. Hanna’s work helps organizations stay ahead of the curve by providing data-driven insights into evolving industry landscapes.