Goldman Sachs warns hyperscalers may spend 100%+ of cash flow on AI with no proven enterprise ROI.

A structural warning is now on the table for the world's most valuable technology companies. The Goldman Sachs AI warning - delivered in back-to-back research notes published in late April and early May 2026 - argues that the four dominant cloud vendors are collectively on course to spend more than their entire operating cash flow funding AI infrastructure buildouts. This is not a market cycle concern. It is a cash flow sustainability question.

The warning arrives as AI spending by cloud companies accelerates beyond prior estimates. Microsoft, Amazon, Alphabet, and Meta are not slowing down - they are accelerating commitments at a pace that increasingly strains free cash flow. At the same time, enterprise adoption of generative AI remains commercially unproven for the overwhelming majority of organizations. This article unpacks the financial mechanics behind Goldman's warning, evaluates the counterarguments from industry analysts, and draws out the strategic implications for enterprises and investors navigating the AI infrastructure era.

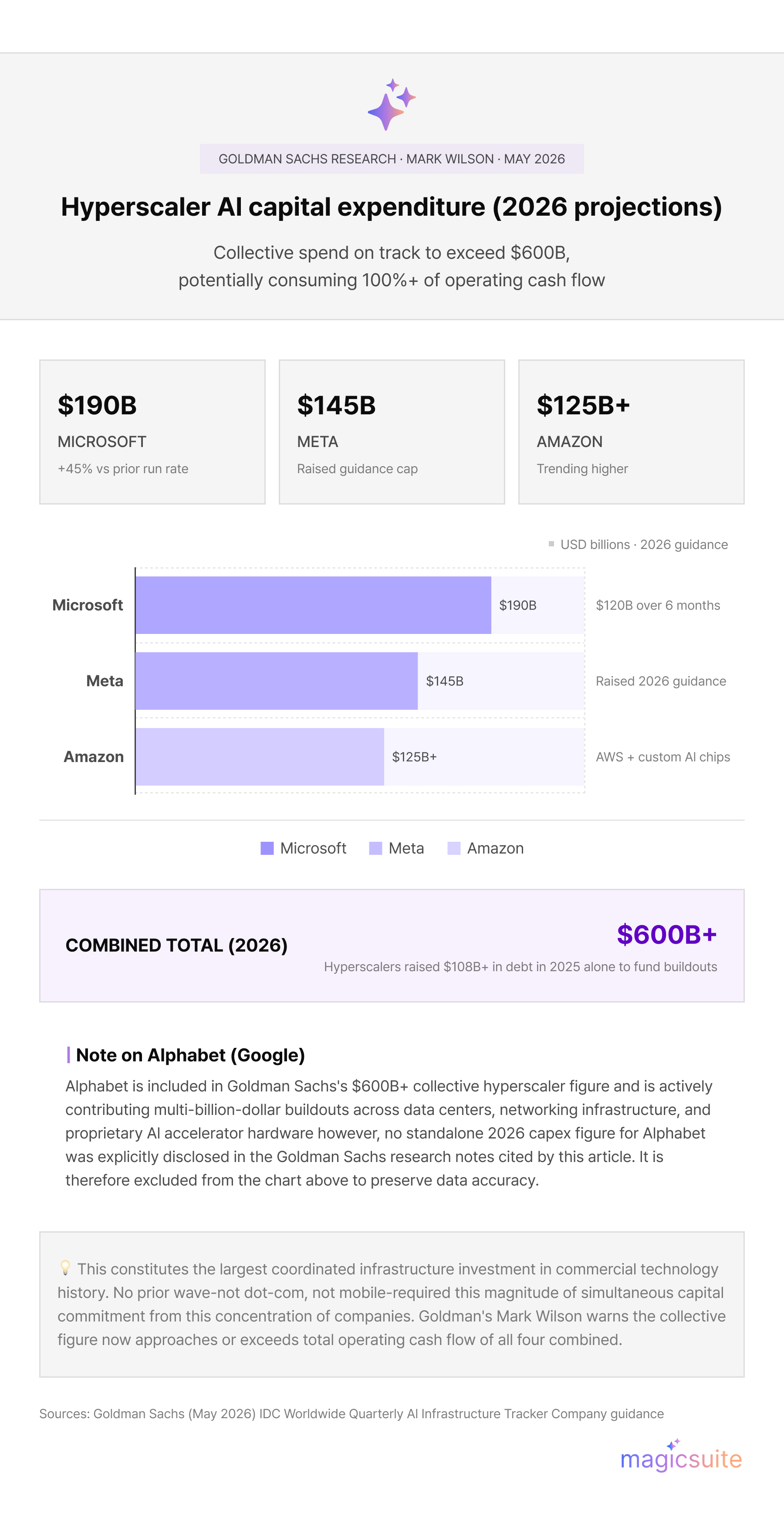

The numbers driving the Goldman Sachs AI warning are not projections - they are current spending trajectories. According to Goldman Sachs partner Mark Wilson's May 3, 2026 client note, Microsoft, Amazon, Alphabet, and Meta are collectively on track to exceed $600 billion in capital expenditures for the year. To put that in context, this figure approaches or exceeds the total operating cash flow these companies generate.

The per-company breakdown confirms the scale of commitment:

This constitutes the largest coordinated infrastructure investment cycle in the history of commercial technology. No previous technology wave - not the dot-com buildout, not the mobile infrastructure era - required this magnitude of simultaneous capital commitment from this concentration of companies.

The scale of AI capital expenditure by Big Tech reflects a deliberate strategic calculus. Each hyperscaler is racing to own the full stack - from custom silicon and data center real estate to foundation model training, inference infrastructure, and enterprise AI services. The underlying logic: the company that controls AI infrastructure at scale will capture disproportionate platform economics.

According to IDC's Worldwide Quarterly AI Infrastructure Tracker, organizations increased spending on compute and storage hardware for AI deployments by 166% year-over-year in Q2 2025 alone, reaching $82 billion for that single quarter. IDC projects the global AI infrastructure market will reach $758 billion annually by 2029. The hyperscalers account for the majority of that spending - confirming this is not a broad-based industry trend but a highly concentrated capital allocation decision made by a handful of companies.

Cloud computing AI costs do not resolve to a single line item. They compound across multiple layers - and each is under inflationary pressure:

The operational impact of these cost structures is not abstract. Gross margin pressure across cloud divisions is emerging as capital intensity rises. For every dollar of AI infrastructure investment, hyperscalers face a multi-year absorption period before incremental revenue offsets incremental depreciation - a dynamic that compresses operating margins in the near term even as long-term revenue potential remains intact.

Goldman Sachs itself has noted that maintaining the returns on capital to which investors have become accustomed would require hyperscalers to realize an annual profit run-rate of over $1 trillion - more than double the 2026 consensus earnings estimate of approximately $450 billion. The gap between required and expected profitability is the core financial tension the market has not yet resolved.

The implication for investors is direct: high AI capital expenditure figures signal both ambition and a sustained period of elevated cost absorption that will not resolve within a single fiscal year.

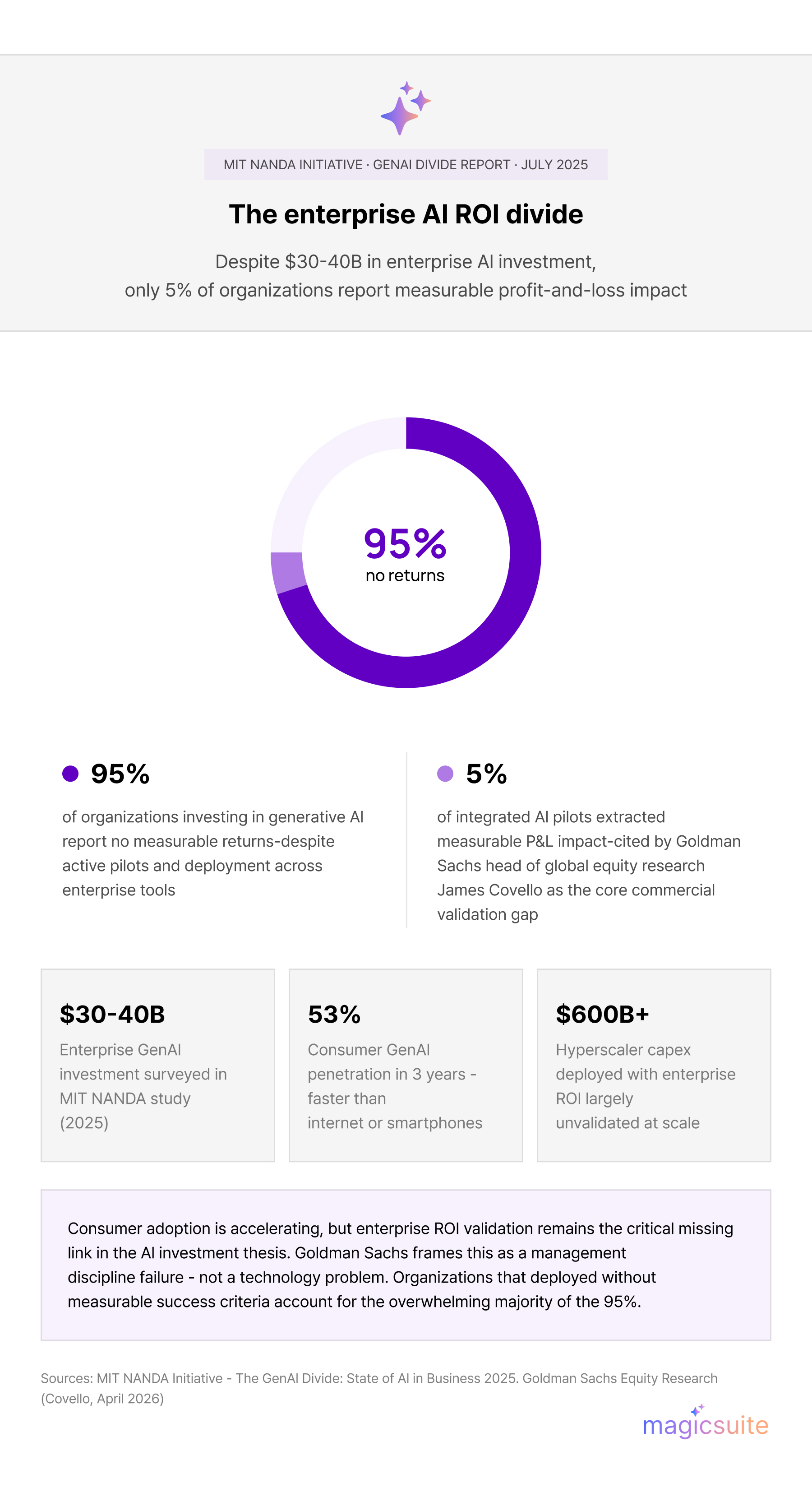

The most analytically significant data point in Goldman's research is not the spending figure - it is the gap between spending and commercial return. Goldman Sachs cites MIT's "The GenAI Divide: State of AI in Business 2025" report, published by MIT's NANDA initiative in July 2025, which found that despite $30–40 billion in enterprise investment in generative AI, 95% of organizations report no measurable returns. Only 5% of integrated AI pilots extracted measurable profit-and-loss impact. This figure does not mean AI is failing. It means the commercial translation of AI capability into enterprise productivity and revenue at scale has not yet occurred in a form that is financially measurable.

James Covello, Goldman's head of global equity research, has maintained this position consistently since 2024. While he conceded in his April 30, 2026 client note that he had underestimated the pace of consumer AI adoption -- particularly given that generative AI achieved over 53% consumer penetration within three years, faster than the internet or smartphones - he reinforced that enterprise ROI validation remains the critical missing link in the investment thesis.

The big tech AI investment risks therefore concentrate around a specific scenario: that hyperscalers continue deploying capital at $600 billion-plus annual rates into infrastructure whose commercial utilization remains unproven, extending the period of cash flow suppression without the corresponding revenue validation that would justify it.

Wilson's note flagged a secondary risk layer: momentum-factor crowding among hedge funds is approaching a five-year high. This signals that institutional capital has concentrated in hyperscaler positions at a level that historically correlates with vulnerability to sharp reversals. Negative data points that could trigger a multi-name reversal include a revenue miss against elevated AI monetization expectations, a capex guidance reduction signaling demand softness, or a high-profile AI project cancellation at a major enterprise customer.

Overinvestment risk is not confined to the balance sheet - it includes narrative risk. If enterprise AI ROI does not materialize within the 12–18 month window that markets are implicitly pricing in, the repricing of hyperscaler multiples could be significant. The structural argument for cloud platforms remains intact, but the valuation cushion at current multiples is narrow.

The defining financial risk articulated in Goldman's May 2026 warning is straightforward but consequential: when a company's capital expenditures reach or exceed its operating cash flow, it can no longer self-fund growth. It must either borrow, issue equity, reduce other investments, or cut spending.

Wilson's warning that the four major cloud vendors are collectively on pace to consume 100% or more of their operating cash flow on AI infrastructure represents a structural inflection point. Free cash flow is the first casualty - and it is the metric that governs dividend capacity, share buyback programs, debt servicing, acquisition flexibility, and reinvestment buffers for non-AI business units.

For Microsoft, which plans to deploy $120 billion over six months, the math is direct: annualized, that rate implies capital expenditures approaching or exceeding its trailing twelve-month operating cash flow. Amazon, with capex guidance already exceeding $125 billion and trending higher, faces a comparable compression. Both companies retain access to debt markets at favorable rates, but prolonged cash flow suppression changes the risk profile of their equity. Notably, hyperscalers raised over $108 billion in debt during 2025 alone to help fund their buildouts - a structural shift from asset-light platform businesses toward capital-intensive industrial utilities.

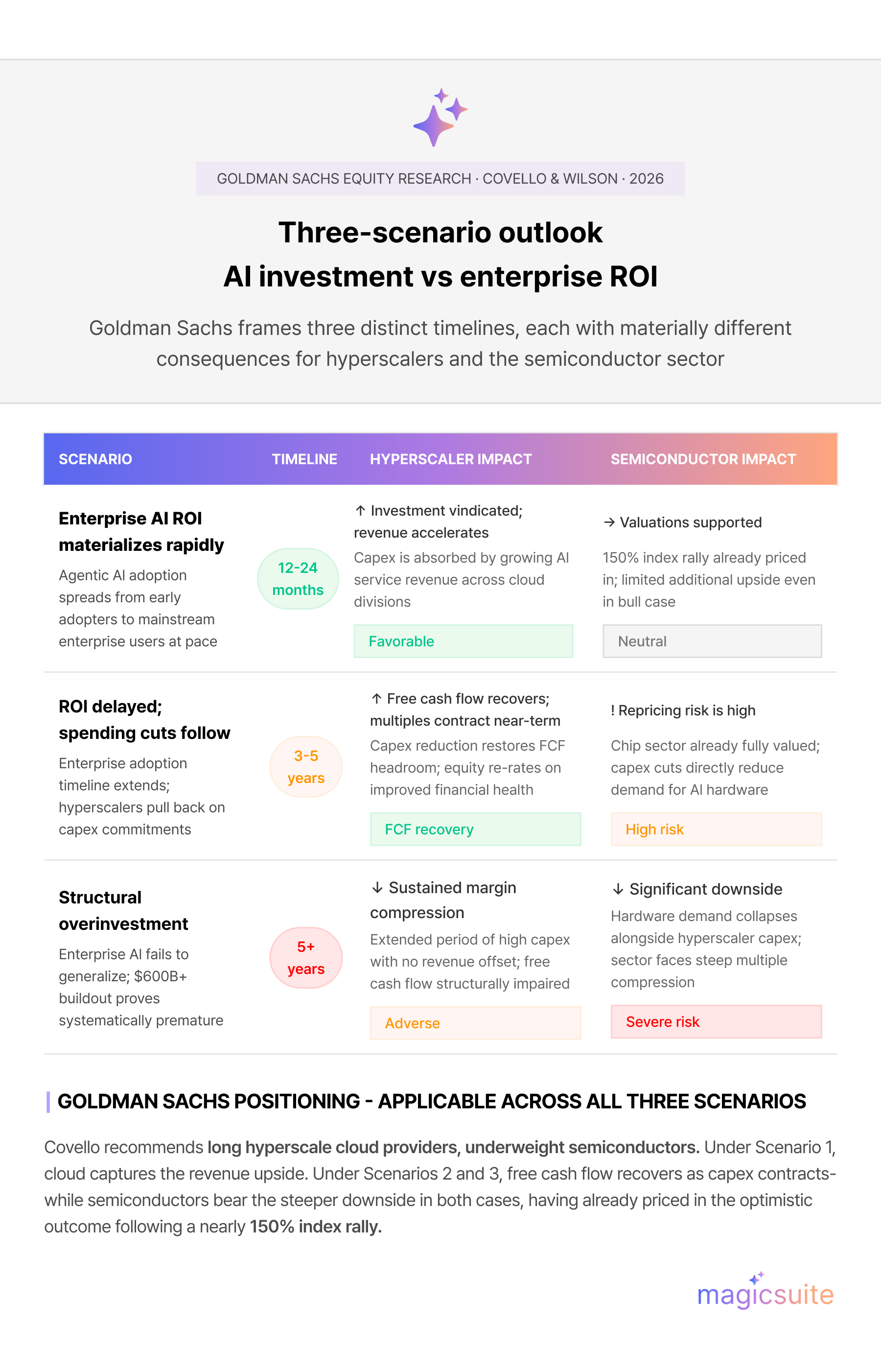

Covello's framing offers a useful analytical lens. He argues that hyperscalers present an asymmetric position relative to the semiconductor sector, with two distinct scenarios both favoring cloud over chips:

Under both scenarios, Goldman's recommendation is to be long hyperscalers and underweight semiconductors - because chip valuations already reflect the optimistic scenario after a 150% index rally, while cloud providers retain upside in either outcome. This positioning reflects a sophisticated asymmetric risk framework, not a simple bullish or bearish call on AI.

SemiAnalysis, a semiconductor and AI infrastructure research firm, published a direct rebuttal to Goldman's framework on April 30, 2026. Their thesis centers on agentic AI - AI systems capable of executing complex, multi-step tasks autonomously - as a structural shift that Goldman's ROI framework fails to capture. Their key arguments:

The upside case rests on whether the productivity gains demonstrated by power users of agentic AI generalize to ordinary enterprise users at sufficient speed and scale.

Both Goldman Sachs and SemiAnalysis agree on the underlying empirical question. The dispute resolves to a single variable: how fast does enterprise agentic AI adoption spread from early adopters to mainstream enterprise users?

If the answer is "within 12–24 months," the infrastructure investment is vindicated and semiconductor valuations hold. If the answer is "three to five years or more," the cash flow suppression at hyperscalers persists without the revenue offset, and Goldman's caution is validated.

Gartner's 2025 Hype Cycle for Artificial Intelligence confirms that generative AI has now entered the Trough of Disillusionment, the stage where inflated expectations give way to implementation realities and organizations refocus on proving measurable value. This pattern is consistent with Goldman's ROI skepticism. Agentic AI platforms, meanwhile, sit at the Peak of Inflated Expectations - a stage characterized by high enthusiasm but not yet validated at enterprise scale.

The Goldman Sachs AI warning is not a prediction that AI will fail. It is a precision financial argument that the current pace of AI spending by cloud companies has outpaced the commercial validation required to justify it - and that the cash flow consequences of that gap are now material. The strategic implications differ depending on your seat at the table:

Luke is a technical market researcher with a deep passion for analyzing emerging technologies and their market impact. With a keen eye for data and trends, Luke provides valuable insights that help shape strategic decisions and product innovations. His expertise lies in evaluating industry developments and uncovering key opportunities in the ever-evolving tech landscape.