Why consumer AI adoption is outpacing enterprise readiness in e-commerce.

Shoppers didn't wait for enterprises to get ready. Over the past year, more than half of U.S. consumers have used AI somewhere in their online shopping journey - comparing products, hunting for deals, or letting an assistant handle checkout. Meanwhile, the brands and retailers on the other side of that transaction are still, by their own admission, in the early innings. This is the core tension defined in Stord's 2026 State of AI in E-Commerce Report: AI-powered shopping has moved from novelty to habit for a critical mass of consumers, while enterprise AI readiness remains shallow, fragmented, and unevenly distributed. This article unpacks what the latest research from Stord, McKinsey, Deloitte, BCG, and MIT Sloan reveals about that gap - and what separates the organizations closing it from those falling further behind.

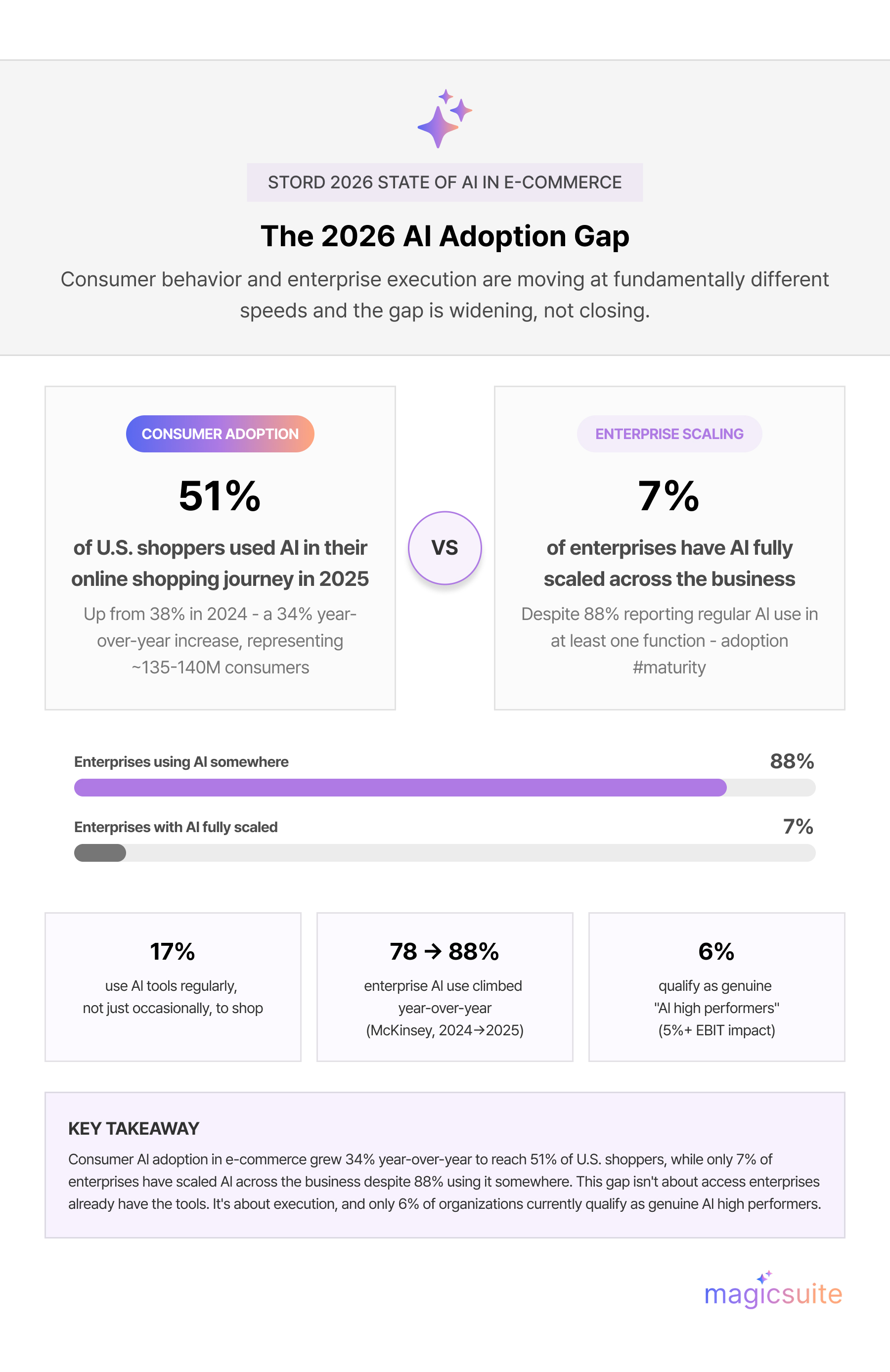

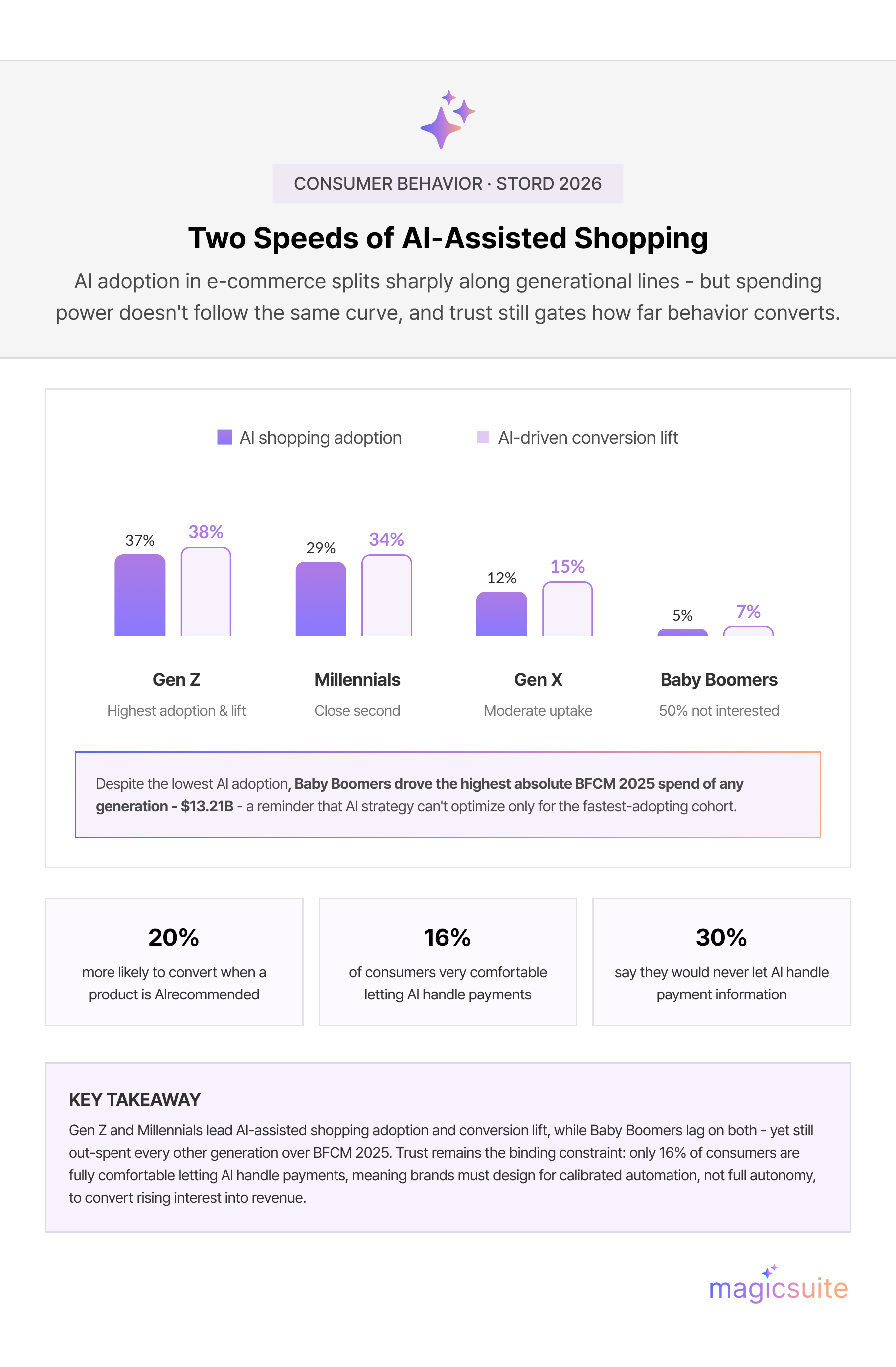

AI in e-commerce is no longer an early-adopter behavior. Stord's proprietary consumer research found that AI-assisted shopping grew from 38% of consumers in 2024 to 51% in 2025 - a 34% year-over-year increase - with 17% now using AI tools regularly to find products. That represents an estimated 135 to 140 million U.S. e-commerce consumers actively relying on AI shopping assistants today. Independent research points the same direction: Adobe's 2026 AI and Digital Trends Consumer Report and Locus's Q2 2026 consumer survey both confirm that AI-assisted discovery, comparison, and purchasing have crossed a mainstream adoption threshold rather than remaining confined to tech-forward early adopters.

The generational divide, however, is stark:

That last point matters commercially. In Stord's own analysis of Black Friday–Cyber Monday 2025 spending, Baby Boomers drove the highest absolute retail spend of any generation ($13.21 billion), even as their adoption of AI shopping tools lagged furthest behind. Brands chasing Generative AI in e-commerce momentum can't simply build for the fastest-adopting cohort; they need to serve a market moving at two very different speeds simultaneously.

The behavioral shift isn't just about whether consumers use AI - it's about how much of the shopping journey AI is starting to absorb. Stord's research describes a shift from the conventional five-step shopping journey (search, compare, choose, checkout, track) toward a compressed two-step "prompt-and-select" model under agentic commerce, where an AI agent handles discovery, comparison, and increasingly, transaction execution.

Early signals of this shift include:

Trust remains the governing constraint. Only 16% of consumers say they're very comfortable letting AI handle purchases and payment information outright, while nearly a third (30%) say they would never allow it. That tension - rapid behavioral adoption colliding with persistent trust limits - is why Stord and other researchers describe 2026 as a year defined less by full automation and more by calibrated human-AI handoffs.

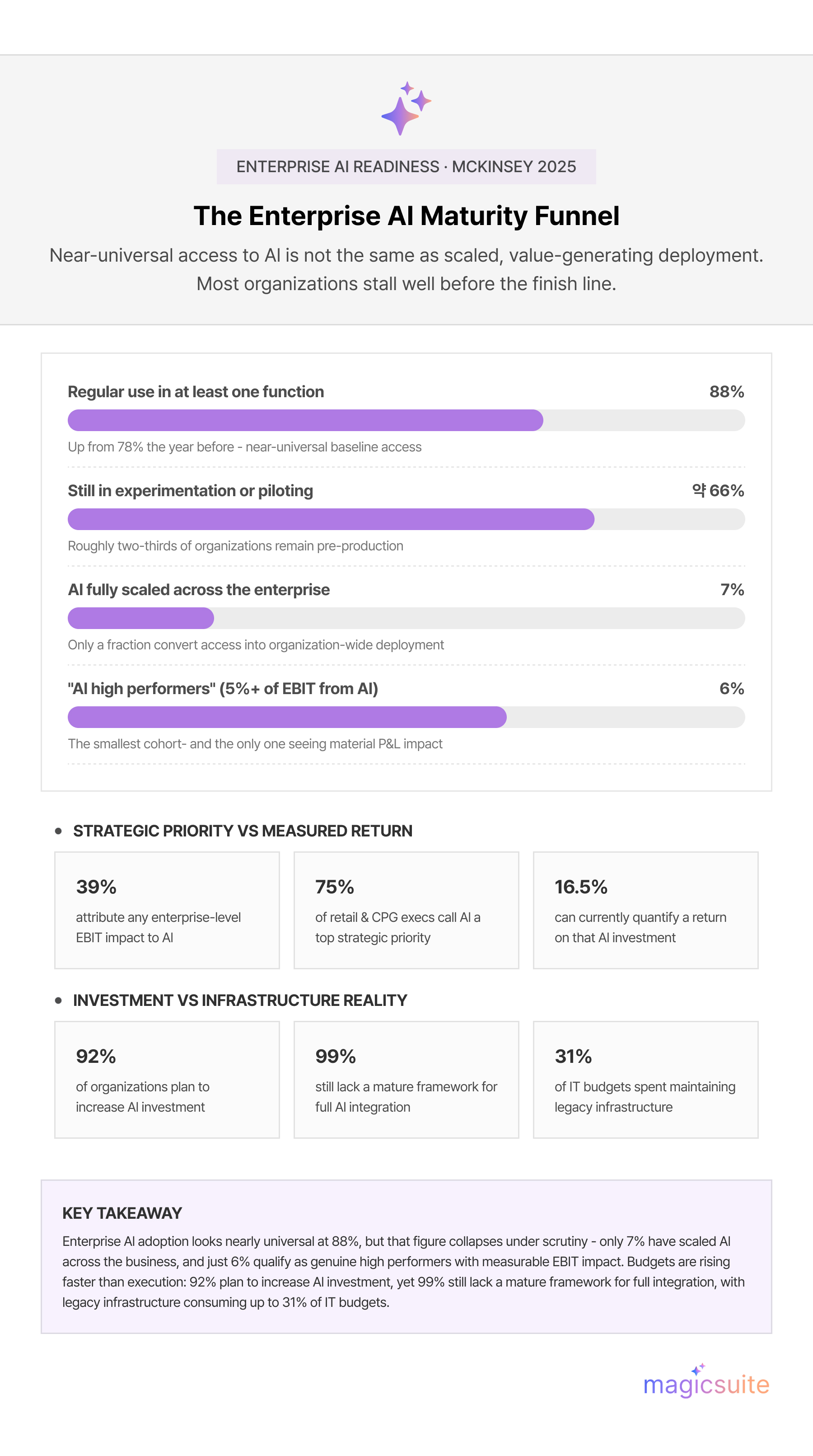

This is where the "outpacing" in the title becomes measurable. McKinsey's 2025 Global Survey on AI - based on nearly 2,000 respondents across 105 countries - found that enterprise AI readiness looks robust at first glance: 88% of organizations report regular AI use in at least one business function, up from 78% the year before. But that headline figure collapses under scrutiny:

Deloitte's 2026 executive survey of 200 retail and CPG leaders found an even sharper version of the same pattern: 75% call AI a top strategic priority, but only 16.5% can currently quantify a return on their AI investment. Deloitte characterizes this as a "say-do gap" - strategy has outpaced operating models, ambition has outpaced investment discipline, and pilots have outpaced production deployment.

Stord's own enterprise data lands in the same range: while 92% of organizations plan to increase AI investment, an estimated 99% still lack a mature framework for full integration across the business. That combination - rising budgets paired with immature execution - is the clearest evidence that AI adoption in e-commerce is a spending story before it's a value-creation story for most brands.

Not every company is stuck in pilot purgatory. Research from BCG, McKinsey, and MIT Sloan Management Review converges on a consistent explanation for why a small group of organizations extracts disproportionate value from AI while the majority stalls.

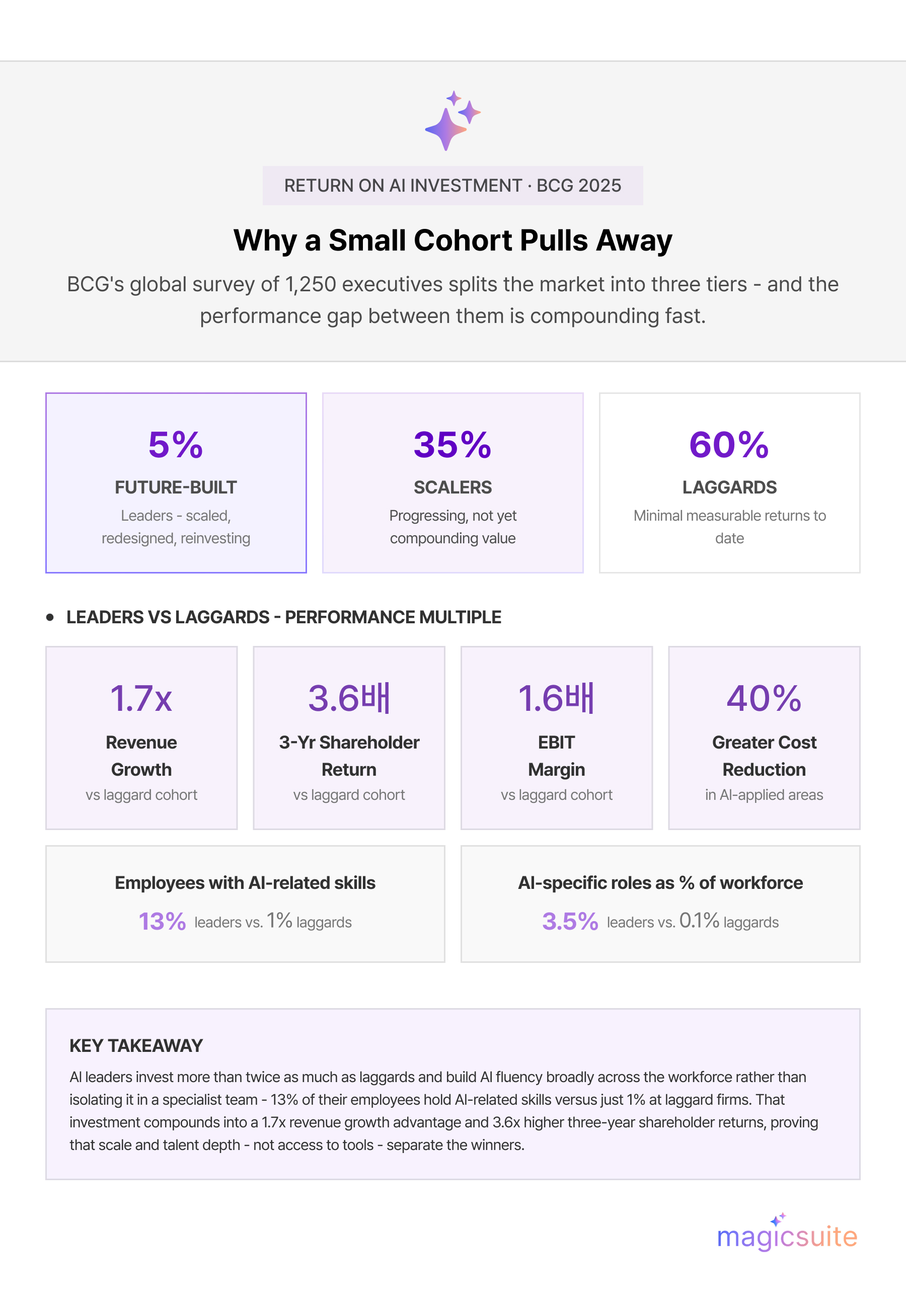

BCG's 2025 AI Value Gap research (a global survey of 1,250 executives) segments companies into three tiers: 5% "future-built" leaders, 35% "scalers," and 60% "laggards" still reporting minimal returns. The leaders separate themselves through:

The financial outcomes are measurable: BCG finds AI leaders achieve 1.7x the revenue growth, 3.6x the three-year total shareholder return, and 1.6x the EBIT margin of laggards, alongside 40% greater cost reductions in the areas where they've applied AI.

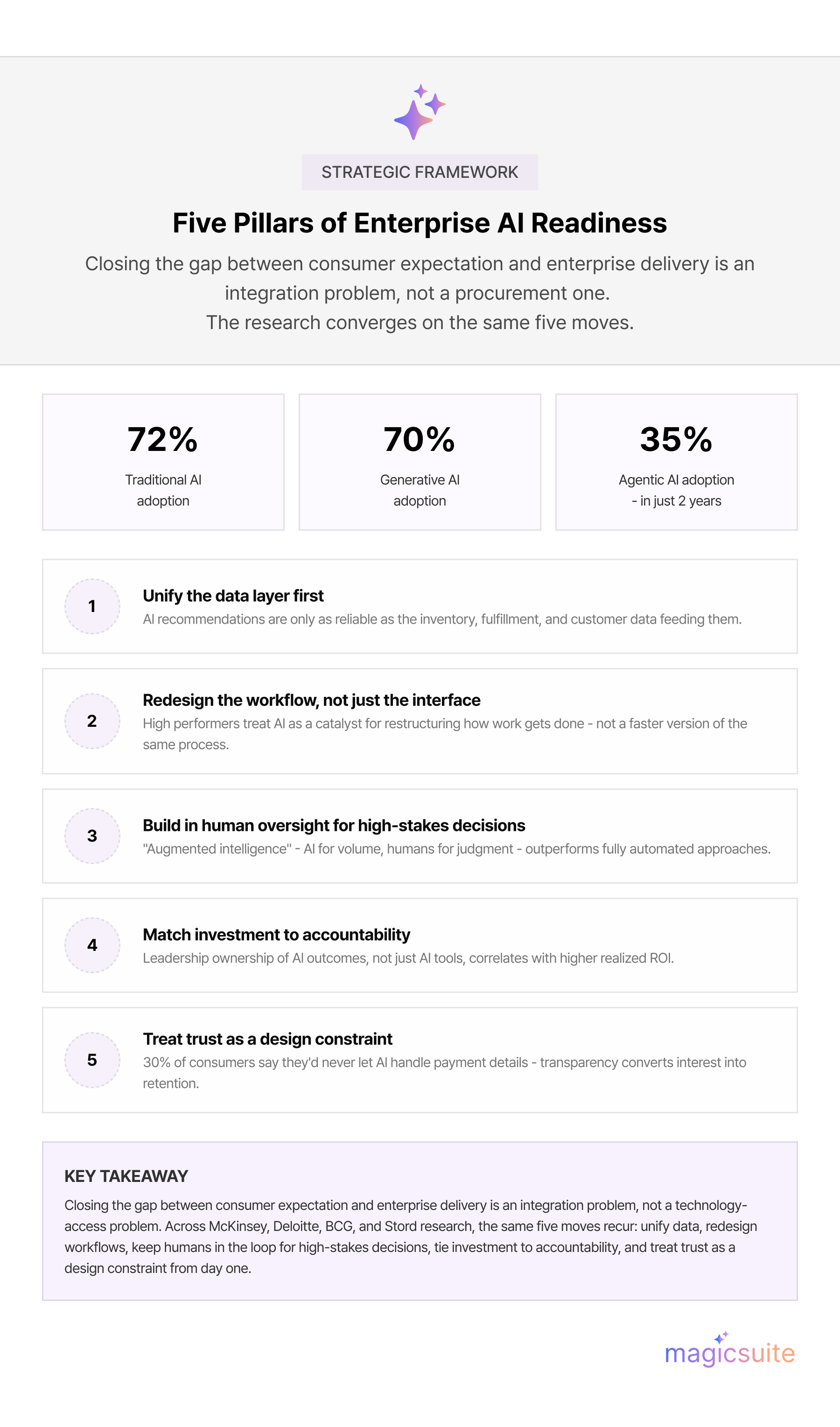

MIT Sloan Management Review's 2025 research with BCG adds an organizational-design lens: agentic AI is scaling well ahead of the governance structures needed to manage it. Traditional AI adoption sits at 72%, generative AI at 70%, and agentic AI has already reached 35% in just two years - but most organizations haven't redesigned decision rights, workflows, or workforce models to match. The practical implication for e-commerce AI specifically: bolting AI onto an unreformed process produces marginal gains at best, while redesigning the workflow around AI's capabilities is where the larger payoff lives.

Enterprises trying to move from pilot to production consistently run into the same set of blockers, and they split cleanly into two categories.

Technical factors:

Organizational factors:

Deloitte's recommendation for closing the say-do gap reflects this same split: put AI strategy in the hands of leaders accountable for outcomes, redirect spend toward use cases that move revenue and margin, and measure scaling - not piloting - as the real indicator of progress.

The pattern holds across use cases. Fast-growing companies derive up to 40% more of their revenue from personalization activities than slower-growing peers, according to BCG's Personalization Index. On the fulfillment side, Stord's research finds that operators using self-correcting, intelligent-routing networks report 65% better service levels and a 15% reduction in logistics costs - meaningful given that last-mile delivery alone accounts for roughly 53% of total shipping expenditure. But these outcomes cluster heavily among the minority that has moved past isolated pilots into integrated, cross-functional deployment.

Closing the gap between consumer expectation and enterprise delivery isn't primarily a technology procurement problem - it's an integration problem. A few patterns emerge consistently across the research for brands serious about digital commerce AI and AI-driven commerce:

The data paints a clear picture: consumers have already decided AI belongs in their shopping journey, and their behavior is compounding quickly - a 34% year-over-year jump in adoption in a single year is a fast curve by any standard. Enterprises, by contrast, are still working through the harder, slower problem of turning near-universal AI access into enterprise-wide value - a transition McKinsey, Deloitte, and BCG all describe as an execution and organizational-design challenge rather than a technology gap.

The long-term implication is straightforward but consequential: the brands that treat 2026 as a scaling year - unifying data, redesigning workflows, and putting outcome accountability in the hands of leadership - will compound an advantage that late movers will find increasingly difficult to close. With AI-powered customer experience now a baseline expectation rather than a differentiator, the competitive question for e-commerce leaders isn't whether to invest in AI. It's whether the organization is structurally ready to convert that investment into measurable, durable performance before the gap between consumer expectation and enterprise delivery widens any further.

Hanna is an industry trend analyst dedicated to tracking the latest advancements and shifts in the market. With a strong background in research and forecasting, she identifies key patterns and emerging opportunities that drive business growth. Hanna’s work helps organizations stay ahead of the curve by providing data-driven insights into evolving industry landscapes.